52. The pitfalls of old-style retirement annuities

Question:I was recently retrenched and now need to access my retirement annuity (RA) to buy a living annuity. I was disappointed by the costs that consumed almost half my meagre growth. There was also a bonus that I would be forfeiting by maturing the investment three years early. Do you have any comments?

Answer: I have received several similar questions from readers who have invested in one of these old-style products with high fees and a limited investment choice.

The product providers like to muddy the waters by providing various bonuses and boosters that you could lose should you change the premium or term.

I will run through some of the checks that readers should perform so that they do not get into this type of situation. I will also show you some of the issues you could consider to improve your lot, should you find yourself in this unfortunate position.

What to watch out for:

How are the charges applied?

The old products levy most of the charges upfront. If you stop paying the premiums at any stage you could be penalised. You should rather go for an investment that applies any costs whenever a premium is paid. This will give you a much higher level of flexibility.

How are commissions being paid?

Are they paid upfront or whenever a premium is received? High upfront commissions mean that less money is available for growth.

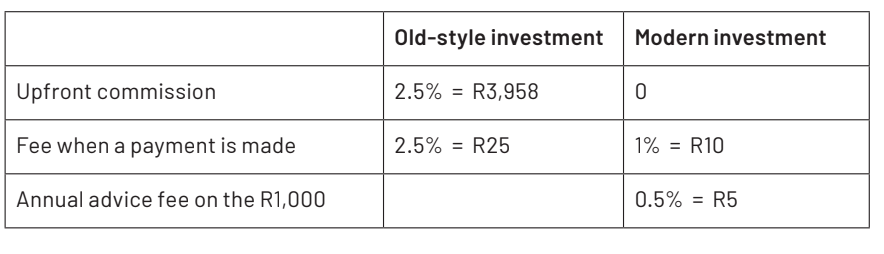

To give you an example, I ran a quote on a R1,000 a month investment into an RA from the same company using an old-school investment and a new-generation one. Below is the income that I could have earned as an adviser .

As you can see, the modern investment pays out a lot less to the adviser and makes more available for growth.

Monitor the investment at least annually

It is vital that you monitor your investments and check in at least once a year to see if you are still on track.

If you can identify a problem early you still have room for manoeuvre. If you reach retirement age with insufficient funds, your options are limited.

Be careful of bonuses and boosters

I like to keep things simple. Many of these products that pay high upfront commissions have a booster that will increase your investment returns if you remain invested and pay the full premium for a particular period. This makes a straightforward comparison of products a bit difficult – which is probably what the product providers want.

Do not make your retirement age later than 55

Fifty-five is the youngest age at which you can mature a retirement annuity.

Insurance salespeople often sell these with an age of 65 to get a higher upfront commission. Having a maturity age of 55 gives you a lot more flexibility. In the case of the person who posed the question, there would have been no forfeiting of the bonus if it was set up for 55.

Investment portfolios: Make sure that you have a decent range of investment portfolios open to you

There are significant differences between the top-performing portfolios and the weaker ones. You do not want to be stuck in an investment where there is very little room for manoeuvre.

So now that we know what to do when we invest in the future, let’s look at the options open to you if you are stuck in a bad investment.

Most of the decisions will require some calculations, as the answers are not obvious.

Understand the impact of stopping the premiums

If you’re in a bad investment, it may make sense to cut your losses and invest future funds in a better structure.

You would need to do the calculations and project them to retirement age to get an accurate understanding.

Change portfolios

The impact of high costs is acutely seen when your investment has performed badly. If you can move your investment into a better performing and cheaper portfolio, you can mitigate some of the damage caused by your initial product selection.

Change provider

You are allowed to move a retirement annuity from one provider to the next. You just need to understand what the costs would be and whether it would be worth the effort.

In conclusion, look carefully at your investments and ensure that you have the right level of flexibility.

If you are stuck in a bad investment, do the calculations to see how you can redeem the situation.