59. What you need to consider before committing to a fixed-interest investment

Question: I am thinking of investing some money in a five-year fixed deposit. Is there anything I should watch out for before making this commitment?

Answer: Without knowing more about your personal circumstances, such as what other assets you have, what your cash flow needs are and how much risk you can comfortably take with your investments, I cannot give any specific advice. What I can do is flag some of the issues you should consider when making any type of investment that will commit you to a five-year fixed-interest investment.

Inflation

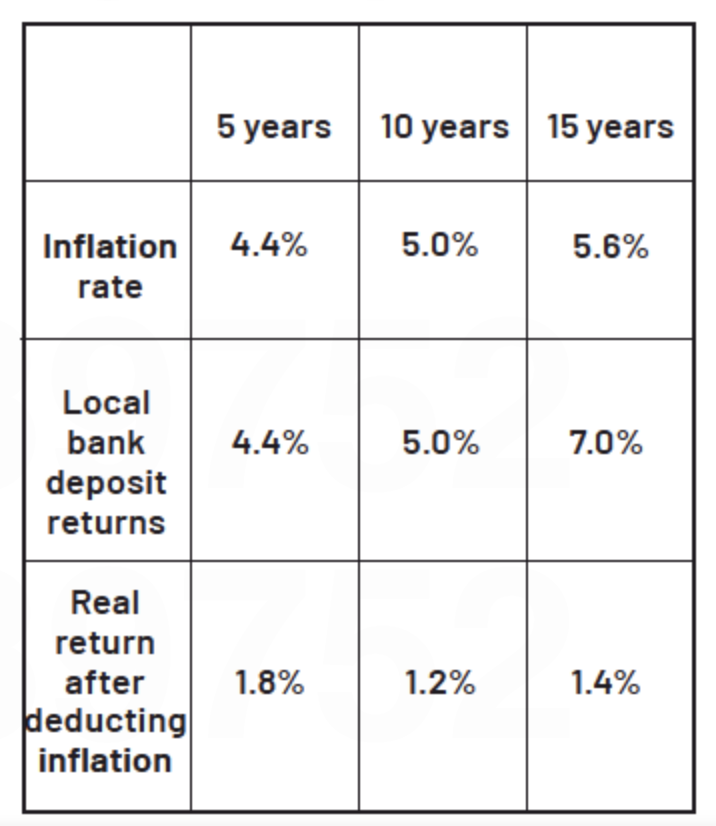

Inflation plays a key part in any investment you make. It is important that you look at the real returns that you are getting once inflation has been taken into account. If you subtract the inflation rate from the investment returns, you will get the real return.

The table below shows the inflation rate over the past five, 10 and 15 years. It also gives the returns you would typically have made from having your money in a bank deposit, in the share market and offshore.

Since 2020, interest rates have been as low as I have ever known them. Inflation was 3.3% in 2020 and 4.5% in 2021. In December 2021, the inflation rate came in at 5.9%. It would seem that inflation is moving upwards, although there are actions being taken to reverse this trend.

Now if you intend committing to a fixed interest rate, you need to make a call on what the inflation rate will look like over the period that you will be invested with a fixed rate. Remember, real returns are important.

Interest rates

Before committing to a five-year investment, give some thought to whether there will be any interest rate movements during that period. You may, for example, be able to get a better deal in a few months’ time if interest rates increase.

We had a 0.25% increase in rates at the end of last year and a number of economists have indicated that we should have more increases.

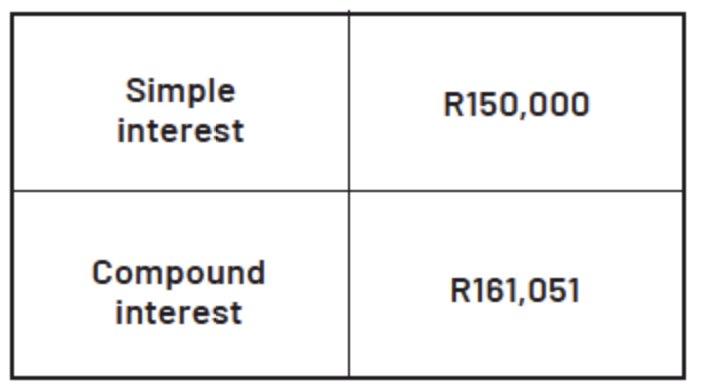

Simple interest is just the interest on your capital, whereas compound interest also gives you interest on the interest you earn. This can make quite a difference to an investment over the coming year. These increases are expected to be relatively small and the overall rate is unlikely to increase by more than 1% over the year. There are a lot of moving parts in these predictions, so the numbers could change.

Compound versus simple interest

When evaluating an investment that quotes an interest rate, you must establish what type of interest is being quoted.

There are two types of interest: simple interest and compound interest. Simple interest is just the interest on your capital, whereas compound interest also gives you interest on the interest you earn. This can make quite a difference to an investment.

For example, if you invested R100,000 at an interest rate of 10%, your investment would be worth the following, depending on whether you received compound or simple interest:

Risk versus return

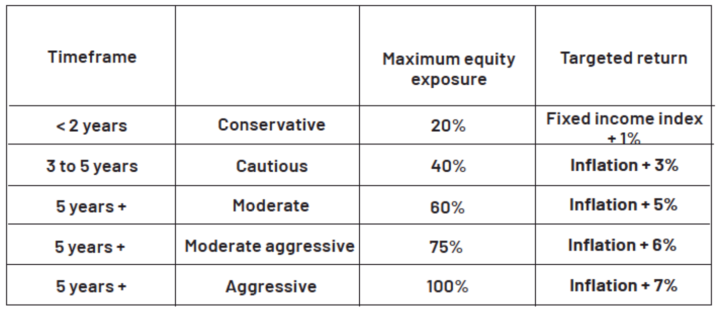

Any investment is a combination of risk and return. The higher the risk, the bigger your return will be. It is important that you understand what your timeframe for the investment is.

I have shared this table on the right before, but it is worth looking at again in the context of this question.

There may be merit in having some equity exposure if your investment time horizon is long.

Tax

You must also take into account any taxes that are payable on the investment.

If you are under 65, the first R23,800 of your interest income will be tax-free and if you are over 65, this amount increases to R34,500. After that you are charged tax at your marginal rate. If you invest in a unit trust, for example, you will pay capital gains tax, which would range from 12% to 18%, on your gain.

Costs

This is something that is vitally important when you’re considering an investment. Are the returns quoted before or after costs are deducted?

If the returns are quoted before costs, you must deduct these costs from that investment.

In conclusion, when you evaluate any investment, look at the following:

- What are the real returns after you have deducted inflation?

- What are the returns after you have deducted costs?

- Do the rates quoted use simple or compound interest?

- What tax will be payable?

- What are interest rates and inflation likely to do over the investment period?