69 - Advice on drawdown rates, and living and life annuities

Question: I am 70 years old and have fallen behind with my bond repayments. I am now facing the possibility of losing my home, but I have sufficient capital in my living annuity. I’ve heard that one can cash in a living annuity if its value is less than R125,000. Is it possible to withdraw R125,000 from a living annuity if the value of the annuity is greater than R125,000?

Answer: Unfortunately, you cannot withdraw additional lump sums from a living annuity as this is part of the legislated structure of the product. You have received certain tax concessions while you were saving up for your retirement and a consequence of that is that two-thirds must be used to pay a regular income to you during retirement.

I do have a possible solution for you, but it will have an impact on the ability of your retirement capital to provide you with a sustainable income for the rest of your life.

You should therefore sit down with a financial planner and rework your cash flows. You need to understand how much money you need to live on each month and what income your living annuity can sustainably provide for you.

Possible solution

Although you cannot make an additional cash withdrawal from your annuity, you can increase the drawdown rate on that annuity for a year or two in order to get the same net effect.

The recommended drawdown for a 70-year-old is 5%. If you go above 8%, you stand a good chance of running out of money in years to come so you should only do this once a financial adviser has modelled your cash flow for you.

You can also go to your mortgage provider and offer to pay the additional amounts owing on your bond by making higher monthly payments for a year or two. This can be funded by increasing your annuity drawdowns to a higher percentage. You can go as high as 17.5%, but you need to be extremely careful at this level.

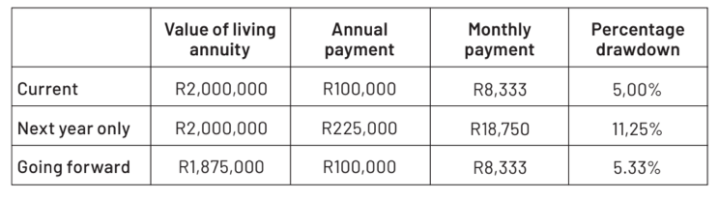

If, for example, you have a living annuity worth R2-million and are taking the recommended 5% drawdown, you will be receiving R100,000 a year or R8,333 a month.

If you increased your drawdown to R225, 000 a year for just the next year, you will have the additional R125,000 you need for your bond. Your drawdown rate will increase to 11.25%. This is summarised in the table below.

As you can see, this withdrawal will increase the effective drawdown rate. (I have assumed that the annuity is growing at a level that can sustain a 5% drawdown after costs.)

Warning

If you are currently at a drawdown level that is above 5%, then you need to be careful as you can end up drawing down too much of your capital.

This can result in you running out of capital to fund your annuity as you get older.

In order to solve this, you could move part of your living annuity into a life annuity.

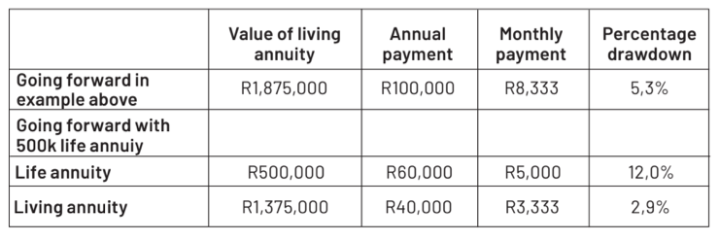

You could get a life annuity that will provide a level monthly income of about R5,000 a month from a R500,000 investment. This could reduce your living annuity drawdown from 5.3% to 2.9%

See the figures we have used in the example of the table provided below.

Remember, whenever you make changes like this, you must get your adviser to model your drawdowns and costs to ensure that you do not run out of money in years to come.

Insider tips

When you are saving for retirement, it often makes sense to invest in several retirement annuities. This will provide you with additional flexibility.

If your retirement annuity at a particular provider is worth less than R247,000, you may cash this retirement annuity in and take the benefit as a lump sum if you are over 55. This additional flexibility would not be there if you combined all your retirement investments into one retirement annuity.

You may want to own several of living annuities instead of combining them all into one large living annuity.

If you had several small living annuities, you could cash in one of them if you have a capital need and the value was less than R125,000.

Similarly, if you needed more income, you could convert one of these living annuities into a life annuity, which would give you a higher income.